{kind=link}

Some individuals can already use Apple Pay Later, with the corporate promising that it’s going to come to “all eligible customers” within the subsequent few months. However whilst you will have the ability to use it quickly, the query is: Must you?

On the floor, it looks like a good possibility. It’s interest-free, there’s no software kind to fill out, there’s no influence in your credit standing, and also you’re coping with Apple quite than a financial institution or finance firm. However there are some things to contemplate …

The way it works

Let’s begin by how Apple Pay Later works.

When you’ve determined what you need to purchase, you apply for the service throughout the app. You’ll be requested how a lot you need to borrow, and prompted to conform to the phrases. Apple then carries out a “mushy” credit score verify, which implies it checks your ranking however doesn’t report the truth that this has been finished, so it received’t be seen to different lenders.

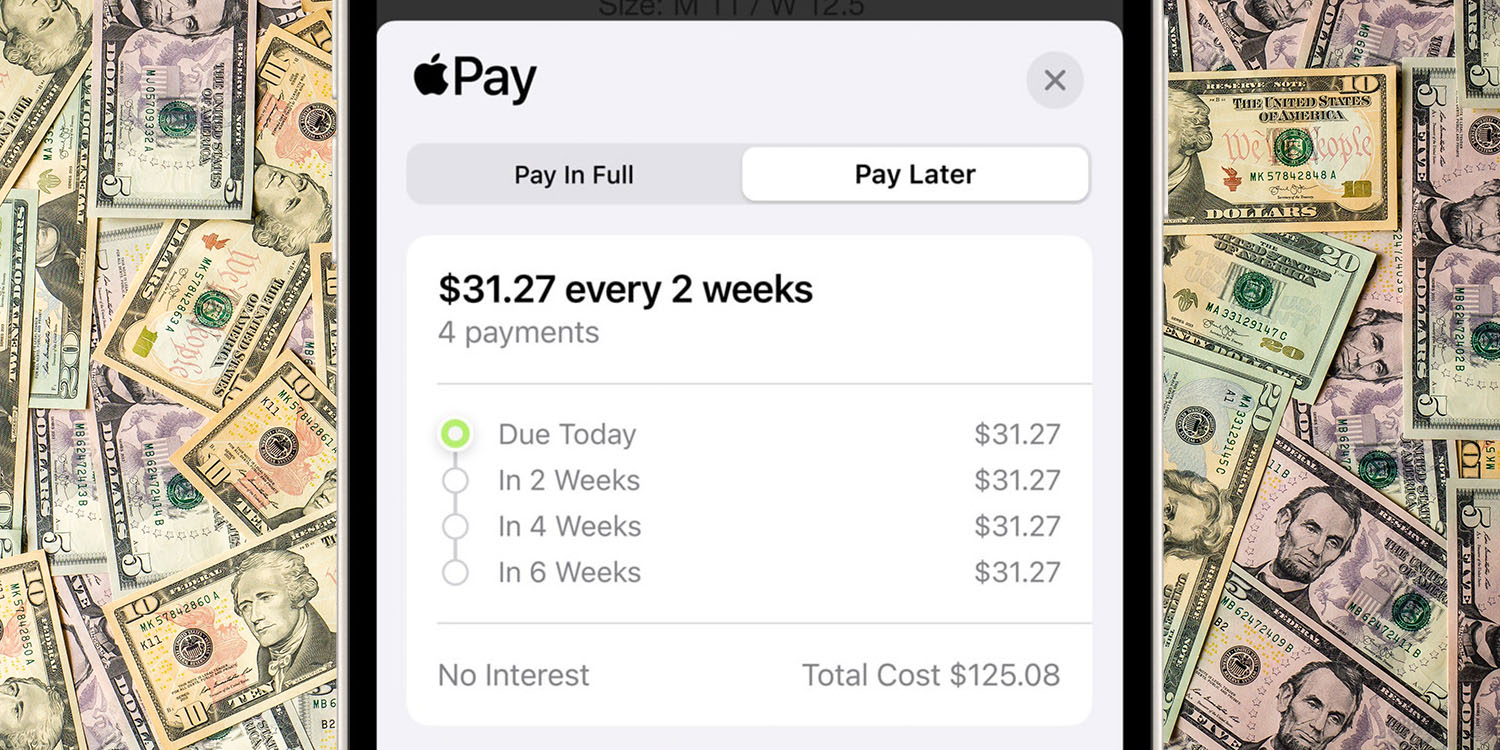

If you happen to’re authorized, then you may go forward and make your buy, choosing Apple Pay because the fee methodology. You’ll then see a brand new tab asking you to decide on between Pay in Full and Pay Later. Choose the latter, and also you’re all set.

To repay the mortgage, you pay in 4 equal installments each two weeks, which is the place the primary of two downsides is available in ….

You’re solely financing 75%, not 100%

That first installment is due on the day you make the acquisition. So 25% of the associated fee needs to be paid instantly, which means that you simply’re solely financing 75% of the associated fee, not 100%.

You’re solely getting credit score for six weeks

The remaining 75% of the associated fee needs to be paid off inside six weeks – which isn’t for much longer than the standard 30-day interest-free interval you get when utilizing a credit score or cost card. But it surely’s really worse than this …

Solely 25% of the associated fee is financed for six weeks

We’ve already famous that it’s important to pay 25% up-front. You then must make funds in two weeks, 4 weeks, and 6 weeks. So the precise credit score durations you might be getting are:

- First 25%: None

- Subsequent 25%: Two weeks

- Third 25%: 4 weeks

- Closing 25%: Six weeks

The utmost quantity you may finance is $1,000

In contrast to credit score and cost playing cards, the place your typical credit score restrict will probably be measured in hundreds of {dollars}, and should run into 5 digits, the higher restrict for Apple Pay Later is $1,000. That will not even purchase you an iPhone, not to mention a MacBook.

You don’t get any rewards

Utilizing a credit score or cost card will often earn you factors, which could be transformed to money or different issues like airline miles. You get these rewards even in case you repay your steadiness in full every month to keep away from curiosity fees. Apple Pay Later, in distinction, provides you nothing.

A credit score or cost card is often a greater deal

If you happen to evaluate the above with a credit score or cost card, you may see that the latter is often a greater deal:

- You’re financing 100% for 30 days, not varied percentages for varied durations.

- You possibly can typically finance a number of thousand {dollars} or extra.

- You get cashback or different rewards for utilizing the cardboard.

So at finest, Apple Pay will get you an additional week – for simply 25% of the full. At worst, you get the identical credit score interval for the complete complete; are restricted to smaller purchases; and get no rewards.

Are there any causes to decide on Apple Pay Later?

If you happen to carry a steadiness in your bank card, then you definately’d pay curiosity in your buy, so Apple Pay Later is a more sensible choice right here, as a result of it’s interest-free as long as you pay it off in full.

The $1,000 restrict may be a constructive factor for some individuals. If you happen to’re vulnerable to over-spending, then the decrease restrict could encourage you to be extra accountable and go for a less expensive mannequin.

Lastly, in case you can’t get different credit score, Apple seemingly has extra relaxed mortgage standards on condition that the quantity of credit score is small, and the mortgage interval each mounted and quick.

But it surely’s not risk-free

As with every “no payment, interest-free” credit score deal, that’s solely true as long as you retain up the funds. If you happen to don’t, then it’s unclear how Apple will deal with the matter, however it’s fully attainable you’ll then run up charges and fees. Moreover, whereas the unique credit score verify was a mushy one, Apple says that it could report fee historical past to credit score businesses – so in case you miss any funds, that seemingly will influence your credit standing.

The golden rule with any credit score is: Solely use it in case you can comfortably afford the repayments, and are assured your monetary place will stay secure for the credit score interval.

What are your views? Are you able to see some other causes to make use of Apple Pay Later? Please share your ideas within the feedback.

FTC: We use earnings incomes auto affiliate hyperlinks. Extra.