{kind=link}

Supply: shutterstock.com/EchoVisuals

There’s an outdated joke about two explorers who encounter a lion. One of many explorers begins placing on trainers whereas the opposite asks, “Are you actually planning on outrunning that lion?”

“No,” solutions the primary explorer, “I solely have to outrun you.”

This quip has turn out to be an apt metaphor for meme shares like AMC Leisure (NYSE:AMC) that survive in horrible industries. By elevating sufficient capital at inflated valuations, these corporations keep solvent whereas their opponents collapse. The very best run of those survivors will finally consolidate the market and flip awful companies into profit-spinning ones.

So, what about GameStop (NYSE:GME)? An organization that has managed to boost $1.7 billion from buyers in its meme-fueled rally?

At first look, the favored inventory has each ingredient of an explorer outrunning their associates. GameStop emerged from the Covid-19 shutdowns with a stronger stability sheet by elevating capital at meme-level costs. No pure-play competitor stays standing.

However a better examination exhibits that the lion is now coming for GameStop itself. The Texas-based video-game retailer has failed to show its consolidated business into significant earnings. In the meantime, the corporate’s efforts to diversify into e-commerce, Web3 and non-fungible tokens (NFTs) have basically failed.

There’s an excellent cause why, final November, I recommended that GameStop wanted Elon Musk to purchase it. Except one thing drastic occurs, shares of GME inventory could possibly be value $11 by 2025… and much much less as time goes on.

GME Inventory: The Present State of GameStop

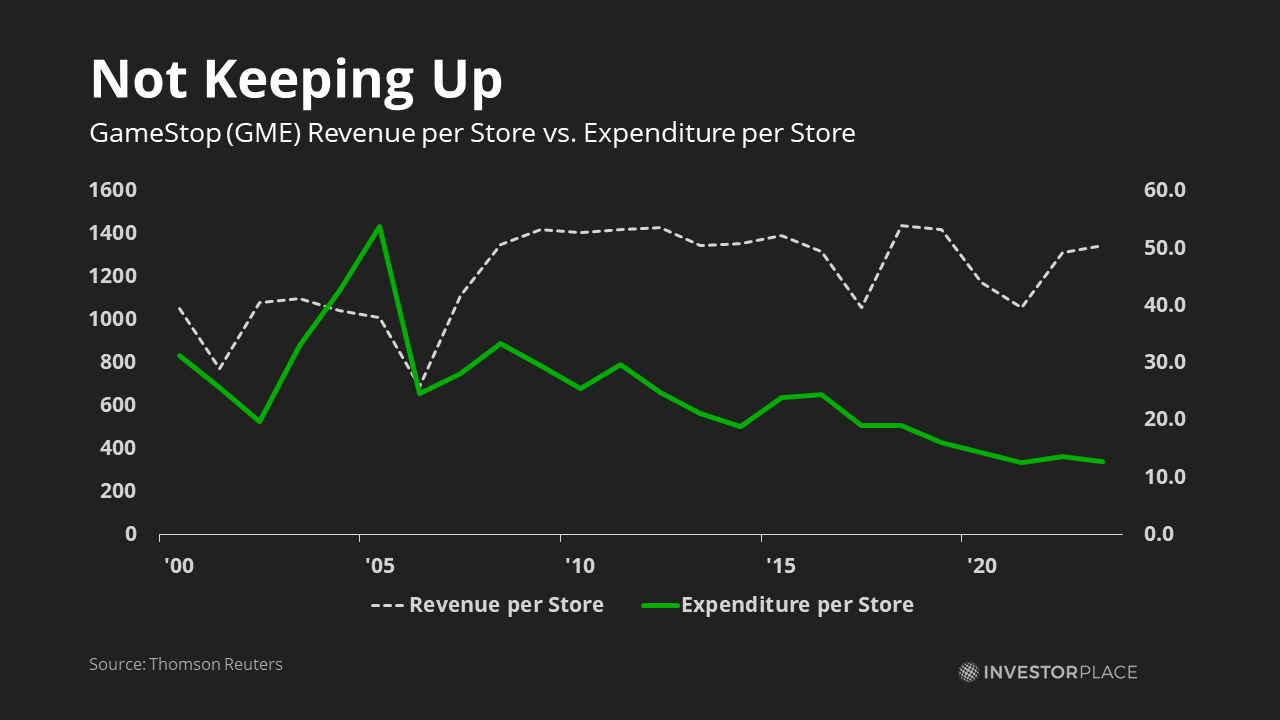

From a monetary standpoint, GameStop is a well-capitalized however underperforming firm. In 2022, the retailer generated solely $52 million in free money circulation from $5.9 billion of gross sales. Dividing by its $1.69 billion invested capital brings us to a 3.1% money return on capital invested, lower than half of its price of capital.

A better examination reveals that even these weak figures aren’t sustainable. In 2022, GameStop inflated its money flows by doing the next:

- Slicing again stock. GameStop generated $230 million by reducing its inventories. It now solely averages 64 days of stock, down from 76 days in 2019.

- Underspending on retailer maintenance. The corporate now solely spends $12,700 yearly per retailer in capital expenditure, down from a median of $22,200 between 2010 and 2019.

- Prepaying fewer taxes. Decrease profitability implies that GameStop generated $172 million in money from not having to prepay revenue taxes.

Meaning GameStop is predicted to publish no less than a $152 million money outflow this 12 months and $156 million the following, lowering its complete liquidity to $1.08 billion by 2025.

Assuming free money circulation begins to normalize after that, a 3-stage DCF mannequin exhibits GameStop’s justified worth in 2025 at roughly $4.30, an 80% draw back.

GameStop Has No ‘Clear’ Valuation

A number of points stand in the best way of this “clear” 2025 valuation.

Firstly, GameStop is shortly turning into the following Blockbuster. Similar-store gross sales are stagnant, even because the agency shuts down its much less productive areas. Digitalization, e-commerce and gaming subscriptions are guilty. Microsoft’s (NASDAQ:MSFT) Xbox Collection S already comes with no disc drive and future generations of consoles could finally observe go well with. The idea that free money circulation will normalize after 2025 is a large leap of religion.

Second, the vary of potential outcomes continues to be pretty massive, because of GameStop Chairman Ryan Cohen. In late 2020, the founding father of e-commerce web site Chewy (NYSE:CHWY) took an activist stake within the video-game retailer with plans to “pivot from a brick-and-mortar mindset to a technology-driven imaginative and prescient.” Though preliminary makes an attempt at revamping the agency’s digital gross sales have fallen flat, a turnaround continues to be not out of the query.

Lastly, retail buyers nonetheless like GME inventory. Shares commerce at 0.99X worth to gross sales as of this writing, increased than Walmart (NYSE:WMT) and almost thrice greater than Greatest Purchase (NYSE:BBY). By the point 2025 rolls round, it’s unclear how this wild card will play out.

Meaning the probabilities for GameStop range significantly. In a bearish case, the agency continues down its cash-burning path, fails to pivot to a digital mannequin and losses speed up as clients abandon bodily video games. On this case, shares ought to commerce underneath money worth since buyers ought to consider losses will proceed. (It’s why 175 biotech firms commerce for lower than their money readily available). On this case, GME inventory may commerce for as little as a $500 million market capitalization by 2025, or $1.64 per share.

In the meantime, a GME inventory bull would possibly assume that the agency finally occurs upon a worthwhile area of interest, say e-sports or digital actuality (VR) gaming. GameStop then turns into the following Twitch and institutional buyers take part on sending shares into the $40 to $50 vary. Assigning a 50% chance of this final result is the one method its justified worth can attain $20 at this time.

The issue with this, nonetheless, is that it entails GameStop exploring these niches, which it’s not doing. The corporate stopped reporting e-commerce gross sales individually and has reportedly laid off employees in e-commerce, engineering and blockchain.

It additionally entails committing tens of millions of {dollars} to analysis & improvement (R&D). GameStop is just not doing that, both. Overheads got here down in 2022 on price cuts.

Meaning my greatest valuation for GameStop solely considers its cash-on-hand, working capital, internet bodily property, intangibles and precise liabilities. Assuming that these figures come to $1.08 billion, $984 million, $650 million, $250 million (i.e. the worth of the GameStop model) and $400 million respectively, the roughly $3.4 billion market capitalization equates to a price of about $11 for 2025.

GameStop: The Downside With a Excessive Share Value

In 2014, GameStop reversed its high-growth acquisition technique to deal with winding itself down. Its high-profile acquisitions of gaming corporations and digital distributors had proved too troublesome to handle.

This less-interesting method of doing enterprise is a surprisingly worthwhile technique. Firms like Coinstar have long-used this tactic to exploit a dying enterprise for money earlier than shutting issues down as soon as nothing’s left. Shareholders are rewarded with good-looking dividends.

Certainly, between 2014 to 2020, GameStop returned about $2 billion to shareholders by dividends and share buybacks. It was an ideal instance of profitably winding down a agency.

In the present day, the retailer has no such luxurious. GameStop’s $20 worth means its enterprise worth now sits at round $4.5 billion, excess of any wind-down worth may produce. And retail buyers would reject that plan anyway. They purchased as a result of they wished GME inventory to “go to the moon,” not a 38-cent dividend.

That’s dangerous information for shareholders. CEO Matt Furlong is attempting to stem losses and switch money circulation round. However we’ve seen this story at Blockbuster and different retailers promoting issues individuals not want. Except GameStop modifications its path, it’s going to face the identical eventual final result.

As of this writing, Tom Yeung didn’t maintain (both immediately or not directly) any positions within the securities talked about on this article. The opinions expressed on this article are these of the author, topic to the InvestorPlace.com Publishing Pointers.