{kind=link}

Historic volatility in regional banking … a reside occasion tonight with Louis Navellier to debate what’s taking place … be cautious of banking right now … the continuing yield curve inversion downside

Since March 1, PacWest Financial institution buyers have misplaced 80% of their capital.

Supply: StockCharts.com

However you see that little rally on the chart during the last couple of days? That small “V”?

It seems, that’s not “small” in any respect…

From bottom-to-top, that was a surge of greater than 130% (utilizing intraday costs, not opening/closing costs).

However earlier than you cannonball right into a regional financial institution inventory commerce, MarketWatch simply reported on a examine suggesting that “shares and actual property are susceptible to a systemic banking disaster that might final months, if not years.”

Six weeks in the past, a examine from the Nationwide Bureau of Financial Analysis concluded that the FDIC bailout of Silicon Valley Financial institution was virtually definitely not an remoted occasion. As a substitute, the examine steered it was symptomatic of a far greater difficulty.

The lecturers behind the examine evaluated practically 2,000 historic authorities interventions of the banking sector from 138 nations, relationship again to the thirteenth century.

Right here’s the bottom-line takeaway from one of many researchers:

We don’t instantly know the way unhealthy issues actually are proper now within the banking system. However we will have a look at the habits of the regulators who presumably know much more than we do about how unhealthy it’s.

And the sample of their responses most carefully matches that of 57 prior crises that tended to extra extreme than common.

Take into account, this conclusion got here out earlier than the First Republic Financial institution collapse. In a follow-up interview with the researchers after that collapse, they concluded “the present banking disaster is rather more extreme than many buyers notice even now.”

Right here’s the bottom-line from MarketWatch:

The professors’ particular prediction is that we’re to start with phases of what they name a “systemic bank-distress episode.”

And right here’s The New York Occasions from just a few days in the past:

Sure, you need to be frightened a couple of potential financial institution disaster…

Our nation’s banking system is at a essential juncture. The current fragility and collapse of a number of high-profile banks are probably not an remoted phenomenon.

Within the close to time period, a dangerous mixture of fast-rising rates of interest, main modifications in work patterns and the potential of a recession might immediate a credit score crunch not seen for the reason that 2008 monetary disaster.

To raised perceive the dynamics behind this misery, in addition to what to do about it, legendary investor Louis Navellier is holding a reside, non-public briefing tonight at 7 PM ET

Right here’s Louis with extra particulars:

In gentle of the previous week’s information, tonight at 7 p.m. Japanese time, I’m internet hosting a LIVE Emergency Banking Briefing.

You see, proper now, my system is pointing to an $8.3 trillion market shock as quickly as September twentieth. I’ll cowl all the small print this night.

Plus, as an added bonus, you’ll be capable of submit any questions you could have for me reside throughout an interactive Q&A session.

Whereas I can’t start to cowl every little thing Louis will reveal, I can let you know to watch out earlier than wading into the regional banking sector proper now.

Sure, for those who’re an completed day dealer, this heightened sector volatility presents a market atmosphere ripe for making fast positive factors (or eye-watering losses for those who guess incorrect).

However for those who’re considering that now is an effective long-term entry level for a buy-and-hold investor, let me share with you Louis’ big-picture takeaway.

For context, Louis has a perspective on this matter that the majority buyers don’t. That’s as a result of he’s an ex-banking regulator – he was an business growth analyst on the Federal House Mortgage Financial institution of San Francisco.

Right here’s his fast take in regards to the banking scenario right now:

I’ve mentioned it earlier than and I’ll say it once more: I’m not a fan of the banks. The reason being easy: I’m an ex-banking regulator.

Right now’s banking disaster brings again some reminiscences.

Again within the late ’70s and early ’80s, the yield curve was severely inverted.

I spent my days merging shedding monetary establishments collectively to make them qualify for Federal Financial savings and Mortgage Insurance coverage Corp. of insurance coverage (now the FDIC handles this). Basically, I’d take the bigger monetary establishment and merge it into the smaller, however would re-amortize its belongings (e.g., its mortgage portfolio) to make the mixed monetary establishment look higher.

Despite the fact that I might by no means repair the mixed establishment’s money stream, I helped them kick the can down the highway as a result of an inverted yield curve is deadly for banks.

I used to “put lipstick on a pig” – and the expertise scarred me for all times.

We’re in the same scenario to the late Seventies and early Nineteen Eighties, in that the yield curve has been inverted since July 2022, that means short-term rates of interest are larger than long-term rates of interest.

It’s no shock that regional banks like First Republic Financial institution bumped into issues.

The actual fact is, so long as the yield curve stays inverted, there may be danger that different banks might fail the Federal Reserve’s capital necessities.

That spells catastrophe for smaller banking shares.

Let’s fill in just a few particulars in regards to the inverted yield curve to verify we’re all on the identical web page

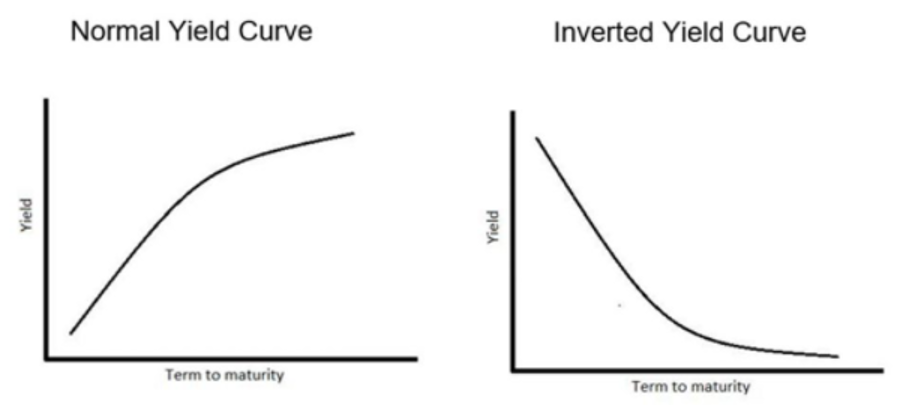

A yield curve is a graphical illustration of the yields of all at present out there bonds – from short-term to long-term

In regular occasions, the longer you tie up your cash in a bond, the upper the yield you’ll demand for it. So, you’d count on much less yield from a two-year bond and extra yield from a 10-year bond.

Given this, in wholesome market situations, we often see a “lower-left” to “upper-right” yield curve.

However when financial situations develop into murky and buyers aren’t certain what’s on the best way, this will change. Particularly, unsure financial occasions tends to flatten the yield curve.

And if the yield curve really inverts, historical past has proven that it serves as a highly-accurate predictor of recessions, although the timing of these recessions is various.

Now, when buyers speak about a yield curve inversion, they’re typically discussing when the two-year Treasury yield climbs above the 10-year Treasury yield.

It seems, this “10-2” inversion has been in impact since final July. Worse, earlier this spring, the hole reached 110 foundation factors, which is the deepest inversion since 1981.

Right here’s a three-year chart of the differential between the 10-year and two-year yields to point out you the inversion and its scope.

Supply: YCharts.com

The impression of a yield curve on regional banks

Usually, banks earn cash by charging debtors larger long-term rates of interest whereas paying smaller rates of interest to depositors. The unfold between these charges is their revenue.

However when the yield curve inverts, or settles across the identical degree, there isn’t an enormous unfold for the banks to make their regular cash. This results in a decline in earnings, which is unhealthy for financial institution buyers.

That is, partly, why Louis stays cautious of banking shares proper now:

Whereas PacWest and the opposite regionals have rebounded in current days, banks have been struggling rather more than only a powerful week…

Actually, it’s been catastrophe after catastrophe over the previous couple of months. I don’t anticipate it getting higher within the close to future.

A Fed charge hike pause just isn’t set in stone… the yield curve stays inverted.

We might not be in a full-on banking disaster, however we’re awfully shut to at least one.

Be a part of Louis tonight at 7 PM ET for extra particulars, in addition to what to do proper now

Additionally, as talked about earlier, deliver your questions. Louis will probably be answering some reside on air.

One query on the market right now is “how lengthy have comparable banking crises lasted up to now?”

Effectively, whereas CEOs like JPMorgan’s Jamie Dimon are saying that this a part of the disaster is now over, the examine we highlighted originally of right now’s Digest begs in any other case.

Again to MarketWatch:

A key characteristic of a systemic banking disaster is the size of time it takes to be resolved. [One of the study’s creators] instructed me that, on common, the 57 prior banking crises most analogous to the present one lasted months, if not years.

That’s an ominous prospect, for the reason that present disaster is lower than two months previous.

As [the study’s creator] put it: “It’s far too early for buyers to say that the disaster is over.”

Backside-line: That is an anxious time for financial institution depositors, and a dangerous time for financial institution buyers. If you happen to’re on the lookout for steering on find out how to navigate right now’s banking disaster from each views, be a part of Louis tonight.

Right here’s he’s with the ultimate phrase:

Over the last banking disaster in 2008, I keep in mind it was hell on earth for many who didn’t put together.

I can’t let that occur to my readers.

Throughout tonight’s livestream, I’ll reveal the 3 issues you are able to do right now to verify your money is protected against any future financial institution failures…

And offer you my whole blueprint, utterly freed from cost.

Click on right here to RSVP, and I’ll discuss to you then.

Have an excellent night,

Jeff Remsburg