{kind=link}

Luke Lango explains why Bitcoin has surged within the wake of banking weak spot … gold almost units a brand new all-time-high earlier than pulling again … what the Low cost Window is telling us

From “down 15%” to “up 18%.”

That’s what Bitcoin has achieved over the previous two-and-a-half weeks as a slew of headlines have rocked the monetary markets.

What’s behind the reversal?

First, two main gamers within the Bitcoin world, Silvergate and Silicon Valley Financial institution, crashed, resulting in Bitcoin sinking. Fears about crypto liquidity drying up resulted in a swift selloff.

Bitcoin fell almost 15% from its early-March excessive as crypto traders ran for canopy.

However because the backstops kicked in (not for Silvergate), traders raced again to the market. Bitcoin has soared almost 40% over the past 11 days, netting out to achieve of greater than 18% since early within the month.

Right here’s how the rollercoaster seems…

Supply: StockCharts.com

Now, some Bitcoin bulls imagine these beneficial properties mirror traders embracing Bitcoin as “digital gold.” In different phrases, when there’s chaos in monetary markets, Bitcoin gives shelter within the storm exterior of the normal banking system.

This would possibly strike you as odd. In any case, isn’t Bitcoin a risk-on asset? Isn’t it extra carefully correlated with riskier know-how shares?

Many traders do maintain this perception. Nevertheless, there’s one other seemingly-conflicting view of Bitcoin as an alternative choice to the greenback and the normal U.S. banking system. That will make it a risk-off asset for these different traders who wish to get away from bother with the greenback and the banking sector.

Our crypto skilled Luke Lango believes a few of this risk-off sentiment is perhaps answerable for Bitcoin’s latest surge, however he thinks one thing else is at play.

How banking failures can goose the crypto sector

Let’s leap to Luke’s weekend replace from Final Crypto:

…This rally is usually concerning the banking sector meltdown killing prospects for inflation and charge hikes and, by extension, bettering prospects for cryptos and danger belongings.

Sizzling inflation and rising rates of interest have crushed risk-asset urge for food over the previous 12 months.

Our bull thesis has lengthy been that in 2023, inflation and rates of interest would cease going up and cryptos would begin going up.

That is already taking part in out as we anticipated.

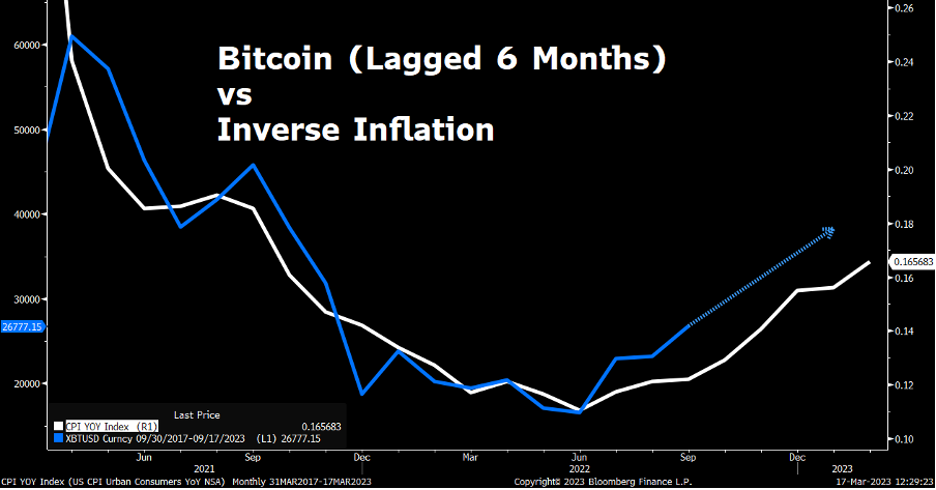

Simply take a look at the next chart. It graphs the inverse of CPI (in white) alongside BTC (in blue), with BTC lagged by six months. Falling inflation is driving crypto costs greater, and this occasion seems like it’s simply getting began.

Supply: Bloomberg

How does the banking sector meltdown affect these traits?

Positively.

Luke factors out {that a} banking failure is massively deflationary.

As a financial institution rolls over, different banks tighten their lending requirements. Credit score dries up instantly, funding in new enterprise slams on the brakes, and shopper spending slows.

Now, multiply that by what’s occurred lately, which isn’t only one financial institution failure, however a string of them.

Put all of it collectively, and Luke sees inflation crashing in our close to future.

Right here he’s reconnecting these macro occasions with crypto:

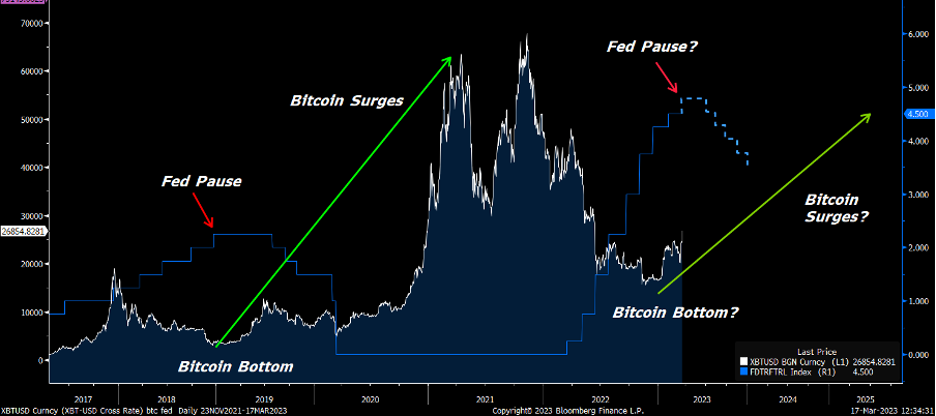

…As inflation crashes and monetary contagion fears unfold, the Fed can be compelled to cease its rate-hiking marketing campaign.

The consensus perception is that it’ll hike charges 25 foundation factors subsequent week earlier than pausing in Could. We predict that is precisely what’s going to occur.

If issues do play out this fashion, that can be very bullish for cryptos, as illustrated by the chart beneath.

Supply: Bloomberg

We stay as assured as ever in our name for a crypto growth cycle in 2023.

In the meantime, there’s one other asset that’s loving the banking sector meltdown

Gold (or ought to we now name it “analog Bitcoin”?)

Yesterday, gold pushed as excessive as roughly $2,029. That took it inside about 2% of its all-time excessive of about $2,075. It has since pulled again to 1,967 as I write Tuesday morning.

Now, on one hand, that is loopy.

Even after crashing, the 10-year Treasury bond yields 3.56% as I write. Even higher, the two-year Treasury yields 4.13%. And you will discover FDIC-insured high-yield financial savings accounts yielding almost 5%.

Why would traders put their cash into gold, that yields nothing?

Concern.

Although Luke simply wrote “this occasion seems like it’s simply getting began,” which might assist risk-on belongings, no less than for now, there are many scared traders on the market who need security.

And as we famous in final week’s Digest, gold performs the position of “chaos hedge” in a portfolio.

If we take a look at the banking sector at this time, regardless that the latest fires have been put out, there’s nonetheless smoke on the horizon.

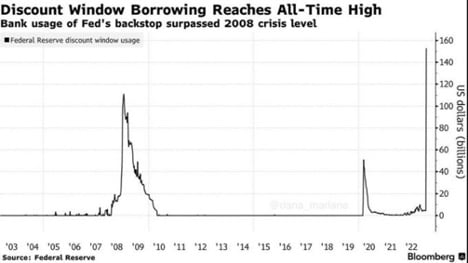

In yesterday’s Digest, we confirmed you this chart of the Fed’s Low cost Window

We’ll clarify the small print of it in a second. First, simply take a look at the spike again within the 2008/2009 monetary market chaos.

Then, discover that our present spike on the far-right facet of the chart is even greater.

Supply: Bloomberg

So, what is that this Low cost Window, and what’s it telling us?

The Low cost Window is the Federal Reserve’s major facility for supporting the U.S. banking system with added liquidity.

The necessity for added liquidity arises when market chaos and/or operational weak spot causes a financial institution money shortfall.

Though the Fed desires to assist troubled banks, it doesn’t wish to be left on the hook if it lends cash to a financial institution that may’t repay the mortgage. So, traditionally, the Fed has required these banks to pony up collateral that has a larger worth than the mortgage itself.

This serves two objectives: 1) it protects the Fed, 2) it makes borrowing from the Low cost Window much less enticing to banks. This makes the Low cost Window a “break in case of emergency” lending facility.

With this context, let’s go to Bloomberg to higher perceive the spike we’re seeing at this time:

To avert additional financial institution runs, a full-blown monetary disaster and potential recession, the Fed determined to make it even simpler for banks to borrow from the low cost window.

It started valuing the collateral it’s supplied in return for cash “at par,” that means at its face worth, quite than observe the standard follow of imposing a haircut. That call was partly taken to ease the stigma banks typically really feel exists when compelled to borrow from the Fed.

The central financial institution wished to make borrowing from it a neater resolution to absorb the curiosity of insulating the broader monetary system and economic system.

It additionally put the dealing with of low cost window loans according to a brand new emergency mortgage facility it had created.

Bloomberg particulars this new facility, known as The Financial institution Time period Funding Program, which got here to be simply weeks in the past within the wake of the Silicon Valley Financial institution (SVB) collapse.

That alone ought to elevate an eyebrow. If the SVB downside was only a one-off, or contained, why would we want a brand-new lending facility past the Low cost Window?

Again to Bloomberg:

Taken collectively, the credit score prolonged by means of the 2 backstops mirror a banking system that’s nonetheless fragile.

Small and midsize banks misplaced billions in deposits that moved primarily to bigger banks and money-market funds following the banking turmoil.

Now, whereas this doesn’t bode properly for the regional banking neighborhood, there’s one other downside popping up, a bit like whack-a-mole.

The following shoe to drop might be within the industrial actual property sector

Business actual property is a highly-levered, $20 trillion trade.

For almost 4 a long time, it has benefited from declining rates of interest.

Out of the blue, that has reversed.

Worse, it has reversed within the wake of the pandemic, during which many companies now not require workers to come back into an workplace. This has lowered demand for workplace house, which has lowered the rental earnings many landlords have obtained.

With this as our background, let’s leap to a latest episode of the Odd Tons podcast.

From co-host Joe Weisenthal:

…Clearly actual property is a highly-leveraged trade in nearly any issue, whether or not it’s malls or workplace buildings or flats or single-family properties. There’s plenty of borrowing, so I believe charges matter. Like each different trade, it’s coping with this reversal of a protracted downtrend.

After which with workplace REITs specifically, everyone knows that working from dwelling continues to be a factor.

Not everybody goes to the workplace on daily basis like they used to. Corporations are lowering footprints.

So, if you’re the proprietor of business property, chances are you’ll be taking a look at a double whammy during which your mortgage is ready to reset, or your industrial mortgage that you simply deliberate to roll over is ready to reset.

On the similar time, due to vacancies, your small business is not so good as possibly it was in 2019. So doubtlessly, a serious stress level is rising for lots of gamers.

You need to surprise how a lot of this “hovering rates of interest” iceberg we’ve seen to date, versus how a lot stays beneath the water’s floor.

However you don’t go from 0% rates of interest to almost 5% on the quickest clip in historical past and never count on to interrupt issues.

The shattering has begun. Let’s see how large it goes.

Have night,

Jeff Remsburg