{kind=link}

Credit score Suisse is the most recent financial institution to be rolling over … encouraging information from this morning’s PPI report … don’t depend on a bull market simply but although … the valuation drawback for shares

This morning introduced excellent news and dangerous information…

As to the excellent news, the Producer Worth Index shocked everybody by displaying that wholesale costs really declined in February.

Estimates had been for a 0.3% improve in costs. As a substitute, they fell 0.1%.

In the meantime, retail gross sales additionally fell 0.4% for the month. That was in step with expectations.

That is welcome information for the Fed and its battle in opposition to inflation, and reduces stress because it mulls its price hike determination subsequent week.

In the meantime, the dangerous information is that issues within the banking sector are intensifying.

On Tuesday, Credit score Suisse introduced it had discovered “materials weak spot” in its monetary reporting course of from the previous few years. This has already been a supply of concern for not simply Credit score Suisse, however the potential domino impact on the broader banking sector.

However then, this morning, the Saudi Nationwide Financial institution, which holds a ten% stake in Credit score Suisse, introduced that it could not present any financial help to Credit score Suisse if issues snowball.

That is troubling information primarily for the European banking sector. However given the interconnected relationship between multinational world banks, that is additionally regarding for U. S. massive banks.

It’s not a foul thought to unfold your deposits over a handful of banks in order that they don’t exceed the $250,000 FDIC insurance coverage restrict.

Now, in mild of the cooler PPI print and the banking chaos, there’s an inexpensive takeaway:

The Fed is about to pause charges.

That might simply occur, sure.

However that doesn’t imply we’re on the verge of a rip-roaring bull market.

Let’s dig into this a bit extra since there’s a rising narrative that “dangerous information is nice information” means the Fed is finished with its price mountaineering, and that’s going to usher within the subsequent nice bull market.

And to be clear, I’m not speaking a couple of market that grinds larger, including, say, 4% or 5% this yr. I’m speaking a couple of full-on, multi-year bullish extravaganza.

Let’s see what some numbers inform us.

What historical past says concerning the beginnings of bull markets

Traditionally, our biggest rip-roaring bull market share one major attribute…

They start when valuations are within the gutter.

This is sensible. For a bull to get pleasure from an extended life, it wants area and time to develop from a child bull right into a ripe, old-aged bull.

One strategy to assess valuations is the CAPE ratio, which is the cyclically-adjusted price-to-earnings ratio.

This indicator appears at a typical price-to-earnings (PE) ratio however makes use of earnings per share over a 10-year interval, not simply the previous one yr. That is executed in an effort to clean out enterprise cycle fluctuations.

So, what’s the connection between CAPE values and bull market beginnings?

My buddy Meb Faber is a revered quant analyst who can reply that query for us.

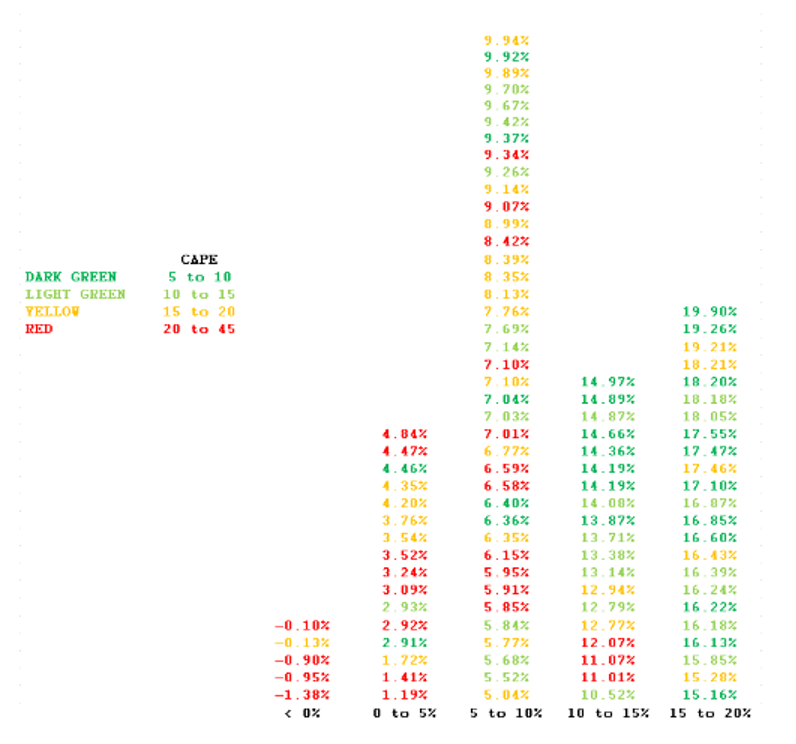

Under is a chart from Meb. Beginning in 1900, the chart reveals preliminary CAPE values and what the following 10-year inventory market returns ended up being based mostly on these beginning CAPE values.

Darkish inexperienced represents the most affordable CAPE beginning years. Pink represents the costliest.

As you’ll see visually, a lot of the “deep inexperienced” beginning years (low CAPE ratios between 5 and 10) find yourself on the best facet of the chart — which means massive 10-year returns.

On the flip facet, “crimson” beginning years (excessive CAPE ratios between 20 and 45) often find yourself on the left facet of the chart — which means low and adverse 10-year returns.

There are exceptions to each rule, however this dynamic performs out constantly sufficient to be extremely useful to a long-term investor.

Don’t fear should you can’t learn the information under. It’s extra essential to concentrate to the colours, with crimson on the left (excessive beginning CAPEs) and inexperienced on the best (low beginning CAPEs).

Supply: Meb Faber

Given this knowledge, what we are able to say is that the chances of a rip-roaring bull market improve when the CAPE ratio begins decrease.

So, what’s in the present day’s CAPE ratio for the S&P 500?

It’s 29.

That places it deep into the “crimson” bucket that features CAPEs between 20 and 45.

Clearly, this doesn’t assist the concept we’re starting a decade-long, rip-roaring bull market.

Now, I do know not everybody views CAPE ratio as a viable indicator.

I disagree, however okay. Neglect CAPE.

What about simply the plain ol’ vanilla PE ratio?

Can we anticipate a raging bull based mostly on the traditional PE ratio?

Just a few years in the past, the analysis store Bespoke analyzed bull markets since 1942 and located that the common bull market begins with a beginning PE ratio of 13.1 and ends with a ultimate PE ratio of 18.9.

From a median perspective, the beginning PE drops to 11.7 and the ending PE drops to 18.7.

And the place’s the S&P’s PE ratio in the present day?

21.

In different phrases, it’s not simply that the S&P isn’t buying and selling at a valuation that’s on par with common bull market beginnings, the S&P’s present valuation is richer than when most bull markets die.

“However Jeff, capital market construction has modified since 1942. PE ranges now are available in a lot larger than they did up to now so your argument is outdated.”

Okay, let’s have a look at this a unique means.

The bull market popping out of the Nice Recession in 2009 was the longest bull market in U.S. historical past

And what was the connection between the PE ratio and the returns of this epic bull?

Nicely, in keeping with knowledge from Guru Focus, the S&P’s PE ratio hit its low round 13.88 in October of 2011. The S&P didn’t attain a PE ratio of 21 (the present PE ratio) till April 2015 — three-and-a-half years after the bull started.

As you may see under, from October of 2011 by April of 2015 the market return was about 84%.

Supply: StockCharts.com

Now, if an investor got here late to the social gathering and wished to hop on the best bull market in U.S. historical past when its PE ratio had hit 21, what was the end result?

Nicely, let’s take our evaluation up till October of 2018.

We’re stopping there as a result of as chances are you’ll bear in mind, the S&P fell 20% from October by Christmas Eve because of the Fed’s tightening coverage. That 20% fall is an official bear market. Let’s say we timed it completely and acquired out in early October.

As you may see under, the S&P’s return from Could 1, 2015, with a PE of 21, to its October 2018 excessive was solely 40%.

Supply: StockCharts.com

Now, a 40% return over about 3.5 years is nice. I’d take that.

However it’s actually not as “rip-roaring” because the 158% return an investor would have loved had he invested in October 2011 when the PE was 13.88 and held till this October 2018 excessive.

Backside line: Beginning valuations matter.

However let’s decrease our bar now…

May we be on the cusp of 40% returns over the subsequent few years?

Nicely, that’s actually extra sensible. However there are massive variations between final decade’s bull market and in the present day.

A comparability between “then” and “now”

Let’s have a look at three variations.

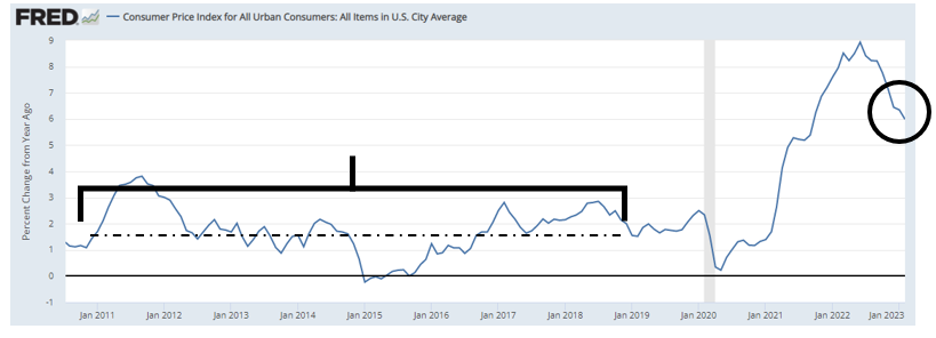

Clearly, an enormous distinction is the CPI.

As we speak’s inflation towers above the sub-2% inflation that marked almost all the post-2009 bull market. The truth is, the common CPI from January 2011 by December 2018 was nearer to 1.5%.

Yesterday, it got here in at 6%.

Supply: Federal Reserve Knowledge

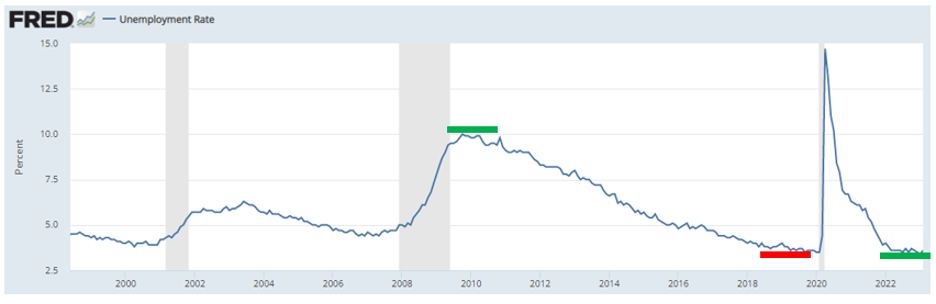

Subsequent, let’s have a look at the unemployment price.

Unemployment is close to file lows in the present day. And whereas which may seem like an excellent factor on the floor, it’s the other.

When almost everybody who needs a job has a job, there’s just one means for this dynamic to go…

The unsuitable path.

See for your self.

The post-2009 bull market began with elevated unemployment that steadily decreased.

As we speak’s unemployment price clocks in on the stage at which the 2009 bull market ended.

Supply: Federal Reserve Knowledge

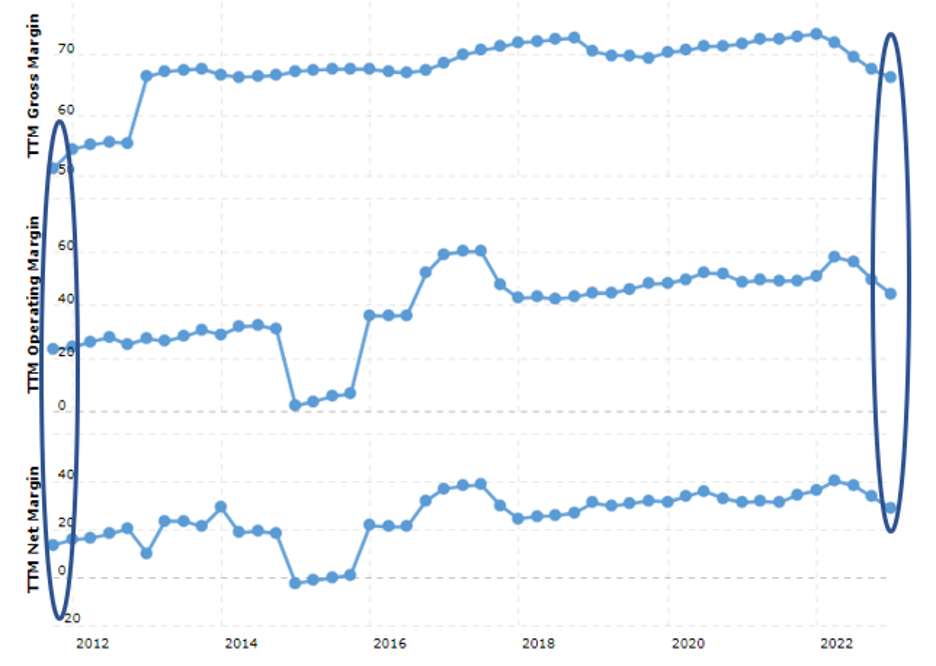

Lastly, what concerning the revenue margins of the businesses within the S&P?

Under, we have a look at a chart displaying the S&P’s Gross Margin, Working Margin, and Web Margin starting in October 2011, extending by January of this yr.

The takeaway is that each one three margin readings are a lot larger in the present day than again in 2011.

Supply: MacroTrends.internet

So, what do all these knowledge inform us?

I’m not making the case the shares are about to hole decrease. I’m additionally not claiming that the market can’t grind larger.

The PE stage is pricey however not nosebleed… inflation is excessive however falling… unemployment numbers can stay low… stress on S&P revenue margins is elevated however has eased…

All of this might assist some inventory market positive factors. However these knowledge don’t assist the concept we’re starting a broad market, decade-long, rip-roaring bull because of a Fed that’s about to do a U-turn.

However…

This doesn’t imply you need to keep away from the market.

Our InvestorPlace analysts are zeroing in on particular corners of the market that they consider supply return-firepower, even when the S&P itself doesn’t.

For instance, Louis Navellier stays extremely bullish on top-tier oil and gasoline shares. Luke Lango has been urging traders to place cash into beaten-down expertise innovators. And Eric Fry is positioning his subscribers in firms which can be main a Renaissance in U.S.-based tech manufacturing.

Whereas the information counsel we’re not in a “rising tide lifts all boats” market, that doesn’t imply sure “boats” can’t do very effectively.

You may consider our funding surroundings as “massive image cautious, small image opportunistic.”

Now, in tomorrow’s Digest, we’ll profile one such alternative that’s been seeing a bunch of triple digit winners during the last yr.

Have an excellent night,

Jeff Remsburg