As of Thursday’s market shut of $167.78, AAPL is buying and selling at a 12.3x a number of on my next-twelve-months EPS estimate (10.8x when excluding next-12m internet money and div).

The important thing instant query for this earnings report is the capital return replace, particularly the deliberate stage of share repurchase essential to realize administration’s said objective of reaching zero internet money stability over time. My comparatively easy mannequin assumes the majority of free money movement (FCF) might be devoted to buybacks, with a smaller allocation reserved for a gradual stage of M/A exercise, dividend funds, and a few debt retirement—because it matures or barely quicker.

The bottom stage of buybacks required to take care of a relentless internet money stability given the projected FCF technology in my mannequin (internet of these reserves talked about) is within the vary of $50–55 billion per yr. On high of that, as a way to deplete the present internet money stability of $163b, a minimum of an extra $150b must be spent in buybacks—barring some big acquisition which I might take into account tragically wasteful. Administration’s statements of doing this “over time” suggests a young supply shouldn’t be a part of the plan, so to maneuver this mountain of further repurchases would take a number of years, a minimum of 3 and certain half a decade. However, front-loading the spending on buybacks (inside what’s cheap and allowed by SEC rules) optimizes the variety of shares retired on condition that I venture an growing share value, maybe after a plateau this yr. Briefly, I am anticipating an authorization to a complete $500 billion in repurchases because the finish of 2012—a rise of almost $300b (together with roughly $115b, $95b, and $75b spent throughout CY18-20 respectively)—and an extra 2 yr extension as much as March 2021. I anticipate additional extensions and extra modest will increase to this system presently annually.

As for the quarterly dividends, I anticipate a rise of 14% from $0.63 to $0.72 per share this yr adopted by related will increase for the subsequent couple of years, which retains a reasonably fixed tempo for the whole quantity spent per yr, after which presumably 20% annual will increase over the next couple of years to get the yield again above 2%, representing solely $2b will increase annually within the whole quantity spent (at the moment $13b) because of the close to completion of the extraordinary repurchase exercise having achieved its supposed impact on the variety of shares excellent. After that, the per share dividend would enhance on the similar charge that FCF grows, boosted by the compounding impact of the recurring repurchases at over $50b per yr.

Not a lot has modified in my mannequin concerning the basic enterprise drivers. After all, market members at the moment are scrambling to rationalize, atone for, or assign blame on final yr’s collective super-cycle delusions—which luckily was by no means a big driver in my mannequin. The primary modifications I’ve made since final yr are increased iPhone ASPs and barely slower unit progress for this yr, partly reversing it for the next cycles with not a lot consequence in the long run. In my view, the affirmation of regular, reasonable progress moderately than fleeting flashes of hyper progress adopted by stagnation or declines is a constructive improvement, as this non-hit-driven path is a a lot preferable strategy to predictable and sustainable progress for Apple and its long-term shareholders.

Bear in mind, the entire beforehand mentioned potential increase from capital return will, for sure, get dismissed by many pundits and naysayers as monetary engineering solely for the aim of artificially supporting the inventory for the advantage of administration compensation (as a result of they as an alternative a lot want to see Apple bail out Tesla and Netflix so these dreamy companies may be funded with zero monetary danger, and be capable of later say, in case these fail, that Apple crippled them). And the unspoken however implied premise is totally appropriate: with no fundamentally-driven progress final result, all of these billions spent on buybacks are nothing however a big waste of the money. The one means it will possibly have a constructive impact is that if the inventory value ultimately rises meaningfully above the value paid (as has been the case for the $176b price of previous buybacks at a mean value of $102 per share). It requires sustainable upside someday sooner or later ideally pushed by fundamentals, or—maybe much less convincingly—by reversing the present market inefficiency.

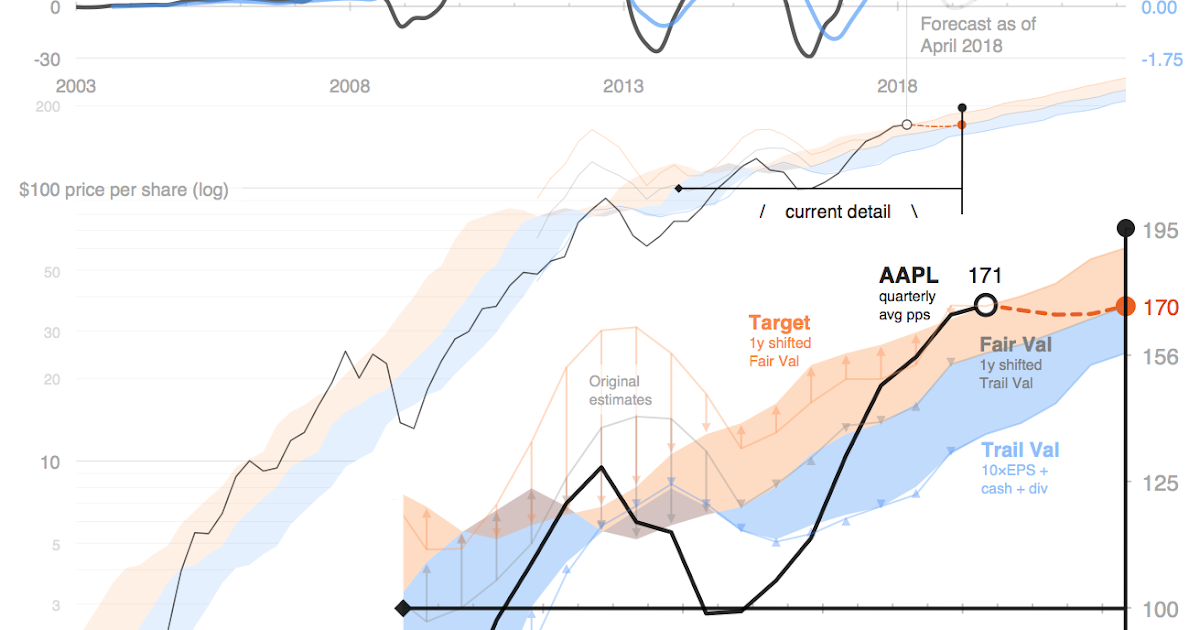

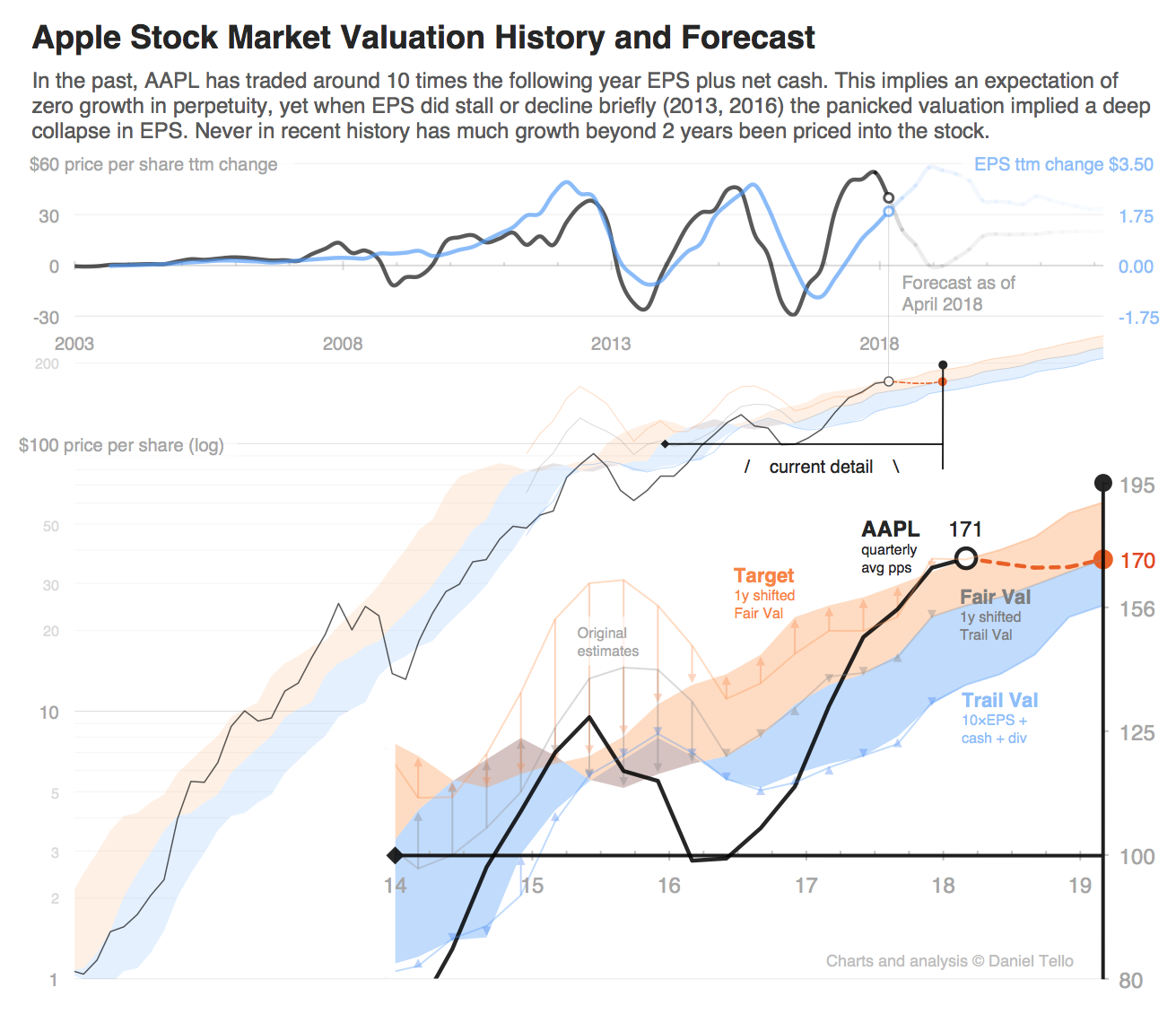

This perennial market skepticism is exactly why I can’t but take into account a extra smart valuation a number of for Apple’s enterprise worth a lot increased than 10 instances earnings. I stay satisfied it can take years of stable efficiency, and coherent, opportunistic and deliberate actions by administration earlier than the market permits the worth of these choices to get absolutely priced into the inventory at a market-comparable a number of. Given my present value goal and long run projection (see chart under), it appears probably that the payoff from these subsequent repurchases might be delayed for a minimum of a few years. That is no downside—the truth is it would be the very best state of affairs—because the full program will take a couple of years to execute, and getting an instantaneous response on the inventory towards a market-comparable a number of earlier than all that funding will get deployed would work in opposition to its potential return.

On this mild, all of the annoying handwringing about “the super-cycle’s bust” and inane claims of “weak iPhone X” are literally a blessing. It actually makes no massive distinction to Apple’s enterprise efficiency—apart from for fiduciary duties—what occurs to all that further unneeded money or what sort of return it will possibly get out of it, nor does Apple rely upon its inventory value to fund its operations—versus another darling corporations. Apple will maintain all of the money it must easily run the enterprise, will carry on investing a wholesome quantity to proceed to innovate and develop, and can return the surplus to shareholders. And it will try this essentially the most environment friendly means—via buybacks. However to us long-term shareholders it does matter an excellent deal the place the inventory goes and what it prices us, as it’s our cash and funding. And to make the very best of it, we might love a dirt-cheap inventory for the subsequent couple of years.

So, I say thanks, pundits and naysayers, for doing our bidding in the course of the subsequent few years (after that I will promptly return to despising your deceitful, manipulative methods). Along with your doggedly dour doomsaying you are serving to Apple assist us grasping AAPL holders get the very best return we are able to on our funding.

Detailed estimates:

3mo ending Mar-2018 Rev($M) GM(%) EPS($) ------------------- ------- ----- ------ Analysts consensus 61,193 - 2.70 Apple information low 60,000 38.0 2.61* Apple information excessive 62,000 38.5 2.77* My estimates 61,702 38.6 2.79 (5.05b shares) 3mo ending Jun-2018 Rev($M) GM(%) EPS($) ------------------- ------- ----- ------ Analysts consensus 52,310 - 2.19 Apple information low (e) 51,000 38.0 2.17* Apple information excessive(e) 53,000 38.5 2.34* My estimates 53,155 38.5 2.36 (4.88b shares) *EPS steering ranges derived from different figures supplied by Apple and diluted shares excellent estimated by me 12m ending Sep-2018 Rev($M) EPS($) ------------------- ------- ------ Analysts consensus 261,874 11.44 My estimates 262,672 11.94 Valuation (fwd-12mo from) EPS($) Y/Y 10x Money* Div Tot ------------------------- ------ ---- --- ---- ---- --- Trailing (Apr-2017) 10.41 22% 104 30 2.52 138 Truthful Worth (Apr-2018) 13.68 31% 137 17 2.88 157 1yr Goal (Apr-2019) 15.87 16% 159 8 3.24 170 * Money per share stability internet of long-term debt

(click on to enlarge)

F2Q18 Income breakdown: iPhone 38,871 (53.0 × $733) iPad 4,327 ( 9.5 × $455) Mac 6,086 (4.35 × $1,399) Providers 8,758 Different 3,659 ( 5.3 × $381 = 2,022 Watch) Earnings assertion: Income 61,702 COGS (37,866) GM 23,836 38.6% OpEx (7,629) OpInc 16,207 26.3% OIE 333 Pre-tax 16,541 Tax (2,481) 15.0% NetInc 14,059 22.8% Shares 5,046 EPS $2.79 (quantities in thousands and thousands besides $ASP, $EPS, and ratios%)

{kind=link}